Sandbox

Sandbox Production

Production

We focus on providing as many payment options for merchants to offer to their shoppers as possible—from cards to wallets to alternatives to bank transfers. In the U.S., the Automated Clearing House (ACH) has long been used to handle bill payments. Our Global Payment Orchestration Platform helps you leverage this popular payment type, giving you the capability to process ACH transactions for both one-time and recurring payments.

U.S. ACH is just one of dozens of local bank transfer solutions that we have made available for you. (For clarity, ACH is available only for U.S. transactions; there are similar tools in other countries, but they have different names, for example, Europe has Single Euro Payments Area, or SEPA.)

Each one is unique, and we encourage you to consider the benefits of each and how they might be helpful for your business. But in this article, we want to highlight the growing (and changing) world of U.S. ACH, and accepting ACH via the payment API.

What Is ACH?

ACH is an electronic payment delivery service for the United States and is an alternative to credit card payments, particularly in B2B settings. This payment method is sometimes referred to as electronic check processing, eCheck, or ECP. While popular for bill payment, ACH can be difficult for online shopping because of the lack of guaranteed funds; however, customers (especially businesses) are demanding this option be available for their online payment systems.

In an ACH payment, money is electronically withdrawn from the shopper’s bank account, transferred over the ACH network, then deposited into your (the merchant’s) own bank account. It works by pushing money between accounts to make a payment, much like direct deposit. Many employers use direct deposit for payroll, to transfer wages from the company account directly to their employees’ bank accounts; ACH works in a similar fashion.

As a merchant, when you accept an ACH payment you gain access to the payer’s bank account—it’s as if they’ve given you their account number and routing number, so that when the transaction happens, the amount due is actually being pulled from their account.

ACH Vs. Debit Cards Vs. Checks

How is ACH different from debit cards and checks?

- With debit card transactions, you also draw funds directly from shoppers’ bank accounts. The main difference between debit and ACH is that your debit-paying customers are afforded the same level of fraud protection that credit-card users get. So if their account is ever hacked or someone commits fraud against their account, they are protected. Debit cards also come with additional safety features, like chips, enhancing the level of security even further. In B2B transactions, where there’s usually an already-established level of trust between the two parties, this is less of an issue.

- With checks, the main difference is that the transfer of funds involves a paper check rather than being handled digitally. The fact that paper is involved introduces the possibility of human error; delays caused by mail processing, check payments are also less reliable, since it can take weeks for a check to bounce.

So, Why Should Your Business Use ACH?

ACH is a good solution for B2B transactions, where it’s usually considered to be a better alternative to credit cards. Why?

1. You’re more likely to get the money you’re owed. Because ACH transactions draw directly from a bank account, there’s no chance of a shopper exceeding their credit card limit or spending more than they actually have. In situations where businesses are buying high-ticket items, ACH removes any doubt about a buyer’s ability to pay.

2. It’s a simpler, more effective payment tool. ACH is appealing to both customers and merchants because of its convenience and ease of use. Plus, ACH transactions can be automated, which makes them appealing to customers since they don’t have to remember(to write checks or run to the post office to drop them off) and the benefit for merchants is (you don’t have to do anything at all!). As an accepting ACH through our payment API makes an already simple transaction even more convenient.

3. It’s less expensive and more reliable than credit card transactions. You already know that banks and credit card issuers charge a fee for credit card transactions. And while there’s still a cost for processing ACH transactions, it’s considerably less. Also, unlike credit cards, checking accounts do not have an expiration date; your shoppers may switch credit card companies multiple times but they rarely switch banks, making ACH a better, more reliable, option.

Here are a few stats if you need more convincing:

ACH Network: Quick Statistics (stats provided by NACHA)

- In 2017, ACH processed 21.5 billion transactions that were valued at over $46.8 trillion.

- B2B transactions increased by 5.6% in 2017.

- 2017 was the third consecutive year volume grew by a billion transactions or more over the previous year.

- ACH’s growth rate in 2017 is its highest since 2008.

How ACH Works

From a processing perspective, ACH isn’t too different from processing credit cards when viewed from the payment gateway process. (For more information about the payment gateway process, including discussion on the entire process of accepting payments, check out our article How To Accept Payments Online: The Complete Guide.)

ACH transactions are supported in all of BlueSnap’s integrations. Whether your business accepts ACH via Payment API or hosted checkout page, the process works like this:

- A shopper makes a request to start the buying process.

- BlueSnap sends a payment request to the bank like an authorization for a credit card.

- The bank validates the shopper’s identity and account information.

- The bank puts a “lock” on the money, which means it’s guaranteed for you, the merchant.

- The bank sends an approval notification to BlueSnap.

- BlueSnap’s processing bank removes the appropriate funds from the shopper’s bank account, pays out the necessary fees for the transaction, and gives you the remaining amount.

This process takes just a coupe of days!

How To Accept ACH In The All-in-One Payment Platform

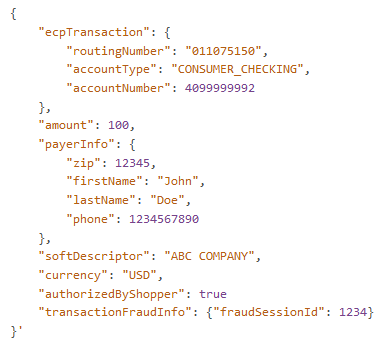

If ACH payments make sense for your business, we provide a simple solution to process transactions via our BlueSnap ACH Payment API. To get started with ACH in the payment gateway API, BlueSnap merchants must first enable the payment method in their account by going to the merchant portal and selecting ACH in the Payment Methods section. In the checkout fields, ask for routing number and account number information.

The example below is all the code you need to roll out ACH payment processing via API:

The account type is flexible, enabling you to process payments from consumer and corporate checking and savings accounts.

We also support ACH transactions for vaulted shoppers, meaning you can create a frictionless checkout experience for your returning shoppers who use ACH. The first time a shopper uses ACH, simply store those details as a vaulted shopper:

When the shopper returns for future transactions, you can easily retrieve their ACH details to pre-populate the checkout page, making it as simple as possible for your customers to complete checkout.

Additional details on our broader Electronic Check Processing (including US ACH) are available in our technical docs.

Ready to start accepting ACH through your payment API?

ACH payments are gaining popularity—make sure your business gives customers all the support they need! For more info, talk to sales.

Related Resources: