Sandbox

Sandbox Production

Production

No matter the size or reach of your company, debit and credit card authorization rates matter. That’s especially true in global eCommerce, where cards are a fundamental pillar of online payments, even as other payment types grow in popularity.

Unfortunately, debit and credit authorizations can fail for a number of different technical or financial reasons, meaning the sale cannot be completed — and for big-ticket items or during high-traffic seasons, that can be an expensive problem. However, many companies don’t even watch this essential payments metric.

In a recent survey, we asked businesses about their global debit and credit card authorization rates, we find that 40% don’t even know what their rates are. That’s a costly oversight, as authorization rates are vital to optimizing your payments.

All the work you do to attract customers to your site, provide a positive shopping experience and encourage them to make a purchase is wasted if the payment gets declined. The good news is that there are ways to increase your debit and credit card authorization rates, which can grow your overall sales and revenue.

Here’s what you need to know about how you can improve your authorization rates, what causes debit and credit cards to get declined and how the right payment processer can support you in optimizing your entire payment process.

How to Increase Debit & Credit Card Authorization Rates

Understanding Transaction Types & the Authorization Process

Reasons Why Debit & Credit Card Transactions Get Declined

How BlueSnap Helps Improve Card Authorization

Card Authorization Process FAQS

How to Increase Debit & Credit Card Authorization Rates

Because the card authorization process has so many moving parts, your best strategy for optimizing your debit and credit card authorizations is to review the different factors that may be causing declines. By targeting the specific reason for that decline, rather than applying a blanket strategy to all declines, you’ll be better able to quickly determine and apply solutions.

Here are our top six actionable steps for raising your card authorization rates:

1. Know Your Current Payments Situation

Before you can begin to improve, you need to know where you stand. Talk to your current payments provider to fully understand which metrics they use, what data is included in your payment reports, what those metrics mean and what your current rates are. If your provider isn’t transparent about this information or doesn’t make it accessible, you may want to consider switching.

It’s important to clarify the nomenclature here. Some providers track authorization rates while others track decline rates, potentially over different time periods. While they’re two halves of the same coin, you can use and assess them differently, so be sure to understand which one is primarily used and what that percentage is. Similarly, make sure you understand what your provider means by payment conversion rates: it can mean anything from the percentage of site hits that turn into a sale to the number of completed transactions after an item is added to the cart.

2. Know Your Shoppers

If you have shoppers in multiple countries, you need to optimize for cross-border payments. Check whether your declined transactions tend to originate overseas or route through multiple countries. If those transactions have lower authorization rates, consider changing your payment solution’s functionality to better account for that geography.

To improve your authorization rates, you need to work with a payments provider that can successfully process your sales as they happen, including across different regions. Otherwise, you’ll see low authorization rates simply because you haven’t set up your payments to incorporate where and how your customers are shopping.

3. Know Your Transaction Meta-Tags

Your processing bank may decline transactions because they don’t match the established meta-tag for that type of transaction. For instance, if you have a recurring monthly payment but you flag it as an eCommerce transaction, then the bank may decline future payments on the grounds of potential fraud. Those systems are in place for customer protection; you just need to know how to use them to your advantage.

Dig through your meta-tags to ensure they align with the transaction type. Transactions with the appropriate tags lead to higher authorization rates. Ideally, your payment provider should have the ability to flag these transactions accordingly to help ensure they are processed accurately.

4. Know Your Data Usage and Requirements

As data and privacy laws loom large, you need to know how to manage your data to work within those new systems. Regulations like Payment Service Directive 2 (PSD2) are all about more carefully processing and managing data to protect consumers, including requirements for payment transactions.

Considering this example, PSD2 requires Strong Customer Authentication (SCA) for businesses accepting online payments processed by a European Economic Area or UK acquiring bank. This means the seller needs to implement two-factor authentication for transactions.

If SCA is not in use for EU transactions, credit and debit card issuers will likely decline the transaction.

Here’s the crucial piece of the puzzle for this and other similar regulations: the more data you can offer the processing bank to verify a transaction, the more likely the bank will approve it. Analyze your data tracking to assess how you can improve your data usage, and thus boost your authorization rates.

5. Think About Your Payment Options

Transactions that are considered more high-risk may also be declined, and large transactions are more likely to raise flags or alerts. Conversely, smaller amounts of money are more easily authorized. For example, you could implement Buy Now, Pay Later (BNPL) or installment payment options to provide customers more flexibility — and let them submit smaller transactions. Or, you could take a service that you sell for one annual payment of $1,200, and break down the offering into smaller, monthly payments.

If you’re thinking of switching to a recurring payments model, you should determine if your payment processor offers the services and functions needed to support that payment option. Do they have the capability to automatically update expired or renewed card numbers? Do they accept digital wallets, which can provide higher acceptance rates through two-factor authentication? If not, you may need to consider another provider that does support the options you need.

6. Know What to Look for in a Payments Provider

Finally, if your payments provider is causing or contributing to your low authorization rates, that payments provider is holding you back and costing you valuable business. You shouldn’t have to settle for lower rates when your business has improved its practices. You also shouldn’t have to search far and wide for useful, personalized advice on improving those rates.

Your payments provider should enable you to identify the root cause of your low card authorization rates and offer strong tips to help you improve them. Similarly, a provider that’s well-versed in laws like PSD2 will strive to document different transaction categories and be fully responsive so that new regulations don’t impact your business success.

You should also dig into the type of payment processing technology your provider uses. If the provider or its associated banks rely on older technology or don’t have a powerful fraud detection system in place, you may see low authorization rates simply because of that. If your provider is causing you soft declines because of inadequate tech, it’s time to upgrade.

The right payments partner will also have tools in place to do everything possible on their end to improve your authorization rates, including powerful fraud prevention, analysis of past declines, device fingerprinting, automatic updates of customer information, transparent data, failover and ongoing analysis of global transaction types.

Understanding Transaction Types & the Authorization Process

Before exploring the details of how transactions are declined, it’s worth a deeper look at how the authorization process works.

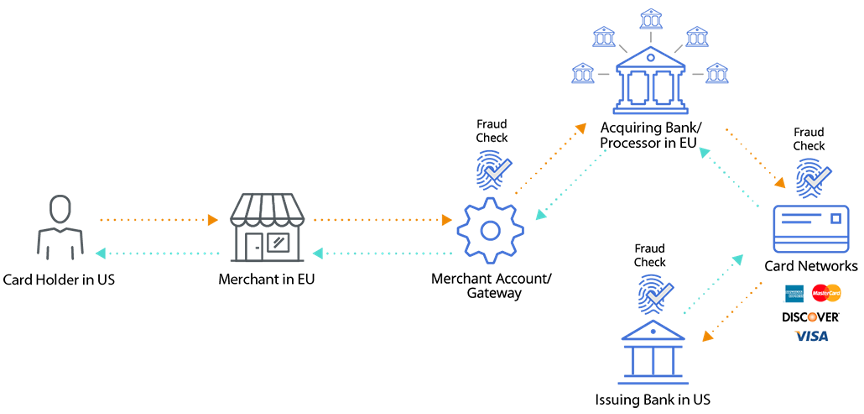

Debit and credit card authorization is obtained by ultimately getting transaction approval from an issuing bank or lender, usually through a credit card processor or financial institution. The process starts whenever a cardholder initializes a transaction with a credit or debit card, the merchant will send a request to the acquiring bank, usually through a payment processor.

The processor’s acquiring bank submits a request to the issuer to review the customer’s account, check if the customer’s card is valid and whether they have the required funds to complete the transaction. If there are no issues and there are sufficient credit/funds, then the transaction is approved. If there is an issue with the transaction, then the request will be declined and the transaction will not go through.

Reasons Why Debit & Credit Card Transactions Get Declined

Insufficient Funds

The most straightforward cause for a decline is when there aren’t enough funds or credit to authorize a payment. This may occur unintentionally when a customer is unaware of their current balance or of other concurrent transactions that lower their available funds/credit. While there’s not much businesses can do to ensure that customers have the required funds for a purchase, you can offer alerts and messages to assist customers with future transactions. Consider a prompt that encourages the customer to provide another payment method or to retry the transaction at a later date, when the original payment method is more likely to have adequate funds.

Changing Data Laws

Whenever countries introduce new data laws or update existing ones, not adapting quickly enough can lower your authorization rates. These laws stipulate new requirements, like SCA, for example, which can muddy the waters when it comes to authorizations. For instance, the authorizing bank will need to sift through the type and origin of each transaction to determine whether it’s required to have that two-factor authentication stamp of approval, or if it’s an exempt transaction. Those complicating factors can lead to an increase in declines, especially if your transactions aren’t clearly flagged.

Poor Fraud Screening

In theory, card declines are supposed to target potential fraud. The higher the likelihood of fraud, the higher the chance that transaction is declined. If you have inaccurate fraud prevention, you could see more declines than necessary if legitimate transactions are flagged as potential fraud, and the transactions get declined to prevent that fraud. Of course, more declines mean a lower authorization rate.

Cross-Border Payments

Cross-border payments, payments that originate from a different country than the acquiring bank, are flagged for declines more frequently than within-region transactions. For instance, a payment using a German-issued credit card that’s processed by a US-only or regional bank is more likely to be rejected than if the acquiring bank were in the same region. Similarly, currency mismatches can cause low authorization rates in out-of-region payments. Generally speaking, transactions across different currencies — especially those with fluctuating exchange rates — are more likely to be declined. It’s best to have local currencies available and to localize the payment process as much as possible.

Customer Account Changes

As card technology evolves, millions of new cards are issued every year to incorporate updated security and new features like contactless payment. That means customer card information is changing more frequently, and if your database doesn’t automatically collect those updates, you may see more frequent declines. For instance, if you have recurring monthly or annual charges but the customer’s card information is no longer accurate, the payment won’t be authorized.

High-Risk Industry or Transaction Categories

If you operate in a high-risk industry — for instance, paid credit score checks or in an industry with more fraudulent traffic — or if you process payments through multiple providers, then your authorization rates will be subject to higher scrutiny and more likely to be declined. The higher the likelihood of fraud, the lower the authorization rates.

Older Technology

If your payment provider or bank uses older technology, you’ll see lower card authorization rates, because older technology fails to address all the above factors. Older tech gateways are less likely to have local routing systems, strong fraud screening, automatic data updates, retry or failover systems, and so on. The latest payment processing software will have systems in place to address common causes of low authorization rates — out-of-date providers won’t.

How BlueSnap Helps Improve Card Authorization

Traditional payment providers often don’t have the technical expertise required to advise your business on the cause of your low rates. At the same time, many payment providers, like Stripe, for example, offer inadequate support around the issue of low debit and credit card authorization rates. As a result, you’re stuck with low rates and no clear path forward.

At BlueSnap, our Global Payment Orchestration Platform is designed to help businesses increase their authorization rates with a single connection to a network of local banks. Our proprietary Intelligent Payment Routing with retries and failover to increase your likelihood of authorization. For example, companies that partner with BlueSnap for processing their digital payments see a 1% to 3% increase in their authorization rate for domestic payments and an impressive 10% to 13% for cross-border transactions.

Your payments provider should enable you to identify the root cause of your low card authorization rates and assistance in helping you improve them. If your payments partner isn’t meeting your needs, it’s time to consider a solution that does.

Card Authorization Process FAQS

What are authorization rates?

Authorization rates are the percentage of transactions that are submitted to and then accepted by issuing banks.

What are decline rates?

The inverse of authorization rates, decline rates are the percentage of transactions that were declined, in comparison to the total number of attempted transactions.

What is an authorization hold?

An authorization hold is a temporary freeze of an approved amount of a cardholder’s money or credit from their account. This hold lasts until the merchant clears the transaction, the transaction is completed or aborted, or the hold expires after a set period of time.

What is a card on file?

A card on file is when a merchant stores a customer’s card and their payment information for future use. Cardholders must first initiate a customer-initiated transaction (CIT) and then authorize the merchant to perform merchant-initiated transactions (MIT) through agreed upon terms for automated billing.

What is a credit card authorization form?

A credit card authorization form is a document granting a merchant permission to charge a cardholder for recurring payments over a period of time. This form is helpful for protecting merchants against chargebacks, as it serves as proof that the cardholder has agreed to a specific number of recurring payments.

What are decline codes?

Decline codes are either usually a number or phrase that specifies the reason for a declined transaction. There is no standardized set of error codes, so they vary from gateway to gateway. Some common reasons for declines are insufficient funds, expired card and Do Not Honor, but different banks and processors may refer to them differently).

What is do not honor?

Do not honor is a generic decline code. It’s used when the issuing bank doesn’t have a specific reason for why a transaction was declined and instead prompts the customer to contact the bank for more information. Do not honor is the most common decline code.

What is a void?

A void is used to cancel a transaction that was previously authorized but before it has been settled. A void transaction will be made in real-time to the card network, telling the customer’s issuing bank to cancel the transaction and approval code. The customer will not be charged for voided transactions.

What is a refund?

A refund debits an amount from the merchant to repay a customer after they have already been charged. After a refund is processed, the customer will see both the original transaction amount and the refunded amount on their balance.

What is an acquiring bank vs. an issuing bank?

The acquiring lender bank, or acquirer, acquires the transaction on behalf of the merchant. The issuing bank, or issuer, serves the customer. It issues credit and manages the cardholder’s funds. These terms apply to where the banks lie within a transaction process. One bank may serve as an acquirer for one transaction, and then as an issuer for a different transaction.

What is the difference between a purchase vs. a pre-authorization and capture?

Purchases happen nearly instantaneously. The card information and amount of the sale are sent to the payment processor, which transmits the information to the card network, and then to the issuing bank to approve the transaction and requested amount. If the transaction is authorized, then an approval code is returned to the merchant from the processor. This process happens in real-time, meaning that within a few seconds, the transaction will be approved or denied by the card network.

Pre-authorizations and captures verify that sufficient credit exists on a customer’s card before a sale is processed. Like a purchase, the transaction is processed in real time, and an approval code is provided to the merchant for the desired amount. While the funds are not immediately debited from the cardholder, the amount is frozen and subtracted from the cardholder’s credit limit. The merchant is guaranteed those funds for up to 7 days and must submit a capture request to complete the sale. While captures can be completed up to 30 days after the original pre-authorization, funds are only guaranteed only for the first 7 days. As a two-step process, pre-authorization and capture offer added protection against fraud and chargebacks.

Frequently Asked Questions

What are cross-border payments?

Cross-border payments, or cross-border transactions, occur when the acquiring bank and the issuing bank are in different regions. When banks process cross-border payments, they perceive them to be riskier than domestic transactions, leading to higher fees and a greater likelihood of being declined.

What is PSD2?

The Revised Directive on Payment Services (PSD2) is a set of regulations intended to establish a clear set of rules for payment providers across the EU and the UK. The intent is to better protect customers when they make electronic payments and to open up competition among providers.

What is Buy Now, Pay Later?

Buy Now, Pay Later, or BNPL, allows customers to make a purchase and receive it immediately, but pay for it at a later time, often over a series of installments via a type of installment loan.

What is Intelligent Payment Routing?

Intelligent Payment Routing is automatic transaction routing between multiple acquiring banks to increase the success rates of payment conversions — including failovers and subscription retries.

How does Intelligent Payment Routing work?

As soon as a customer submits payment, after going through fraud checks, a payment service provider with Intelligent Payment Routing will consider all the transaction’s applicable criteria. The technology will instantly determine which acquiring bank has the highest possible success rate and will route the transaction appropriately.